American domestic debt is just $ 18t, hostage rates are cruel, and lack of bitcoin supply is faster. Is the old way of money breaking?

Real estate is slow – fast

Over the years, real estate has been one of the most reliable methods for making wealth. The value of the house usually grows over time, and the ownership of the property has long been considered a safe investment.

But right now, the housing market is showing signs of recession unlike anything seen in years. The houses are sitting in the market for a long time. Sellers are cut in prices. Buyers are struggling with high mortgage rates.

According to recent data, the average house is now selling for 1.8% below the price asking – the biggest discount in about two years. Meanwhile, the time it takes to 56 days to sell a typical house has increased for the longest time in five years.

In Florida, the recession is even more pronounced. In cities like Miami and Fort Lauderdale, more than 60% Listing They have been unceasined for more than two months. Some houses in the state are selling for more than 5% from their listed price – the most discounts in the country.

At the same time, Bitcoin (BTC) is becoming a rarely attractive option for investors seeking a rare, valuable property.

The BTC recently hit the all -time high of $ 109,114 before pulling back by $ 95,850 by 19 February. Even with DIP, BTC is still Above More than 83% in the previous year, inspired by an increase in institutional demand.

Therefore, since it becomes difficult to sell real estate and becomes more expensive for itself, can Bitcoin emerge as the last store of the price? Let’s know.

From scattering hedge to liquidity trap

The housing market is experiencing a sharp recession, high mortgage rates, inflated in domestic prices and reduces the fall in liquidity.

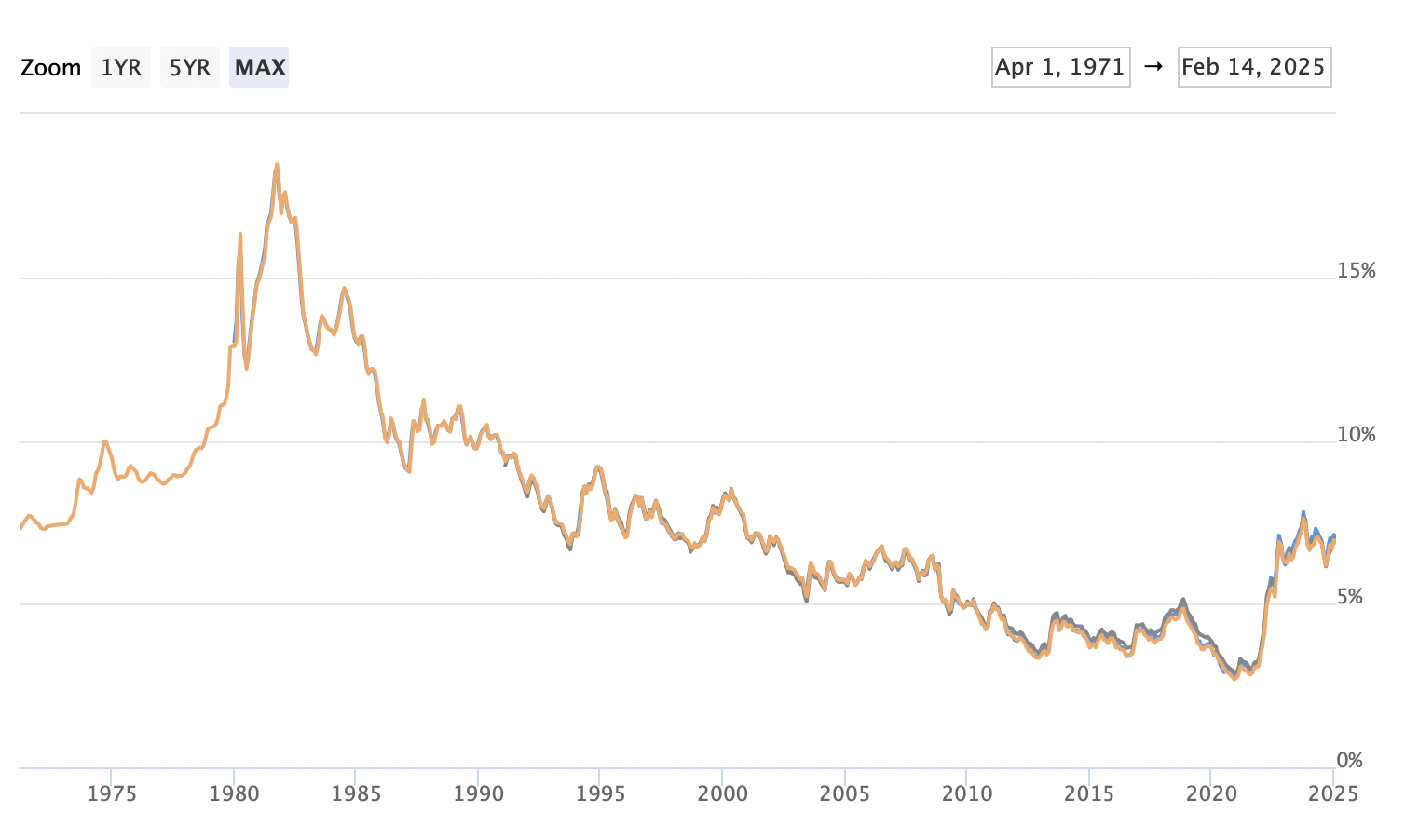

Average 30-year mortgage rate remains High at 6.96%, opposite 3%-5%rates before epidemic.

Meanwhile, the price of the middle American home-selling has increased by 4% year-on-year, but this growth has not been translated into a strong market-the pressure of reference has subdued the demand.

Many major trends reveal this change:

- The average time for a house to go under the contract has jumped up to 34 days, a rapid increase from previous years, is a cooling market signal.

- A full 54.6% houses are now sold below their list price, not seen in a level years, while just 26.5% above. Sellers are forced to adjust their expectations rapidly as buyers take more advantage.

- The middle sales-to-list price ratio has fallen to 0.990, which shows a decline in strong buyer negotiations and seller power.

However, not all houses are equally affected. Properties in prime locations and move-in-redi positions continue to attract buyers, while in less desirable areas or renewal that are facing standing discounts.

But with an increase in the cost of borrowing, the housing market has become very low. Many potential sellers are not ready to participate with their low-fixed-by-fixed mortgage, while buyers struggle with high monthly payments.

This deficiency of liquidity is a fundamental weakness. Unlike bitcoins, which can be traded 24/7 with close-instant execution, real estate transactions slow, expensive and often finally occur in the final months.

As the economic uncertainty looks for more efficient reserves of gender and capital value, obstacles in the entry of real estate and sluggish liquidity are becoming major losses.

Many houses, very few coins

While the housing market struggles with increasing inventory and weakening of liquidity, bitcoin is experiencing contrast – squeezing a supply that is promoting institutional demand.

Unlike real estate, which is affected by the development of debt cycles, market conditions and supply, the total supply of bitcoins is permanently overshadowed at 21 million.

The complete lack of bitcoin is now colliding with increasing demand, especially from institutional investors, strengthening the role of bitcoin as a long -term store of value.

The approval of the spot bitcoin ETF in early 2024 triggers a huge wave of institutional flow, which dramatically transfers the supply-brain balance.

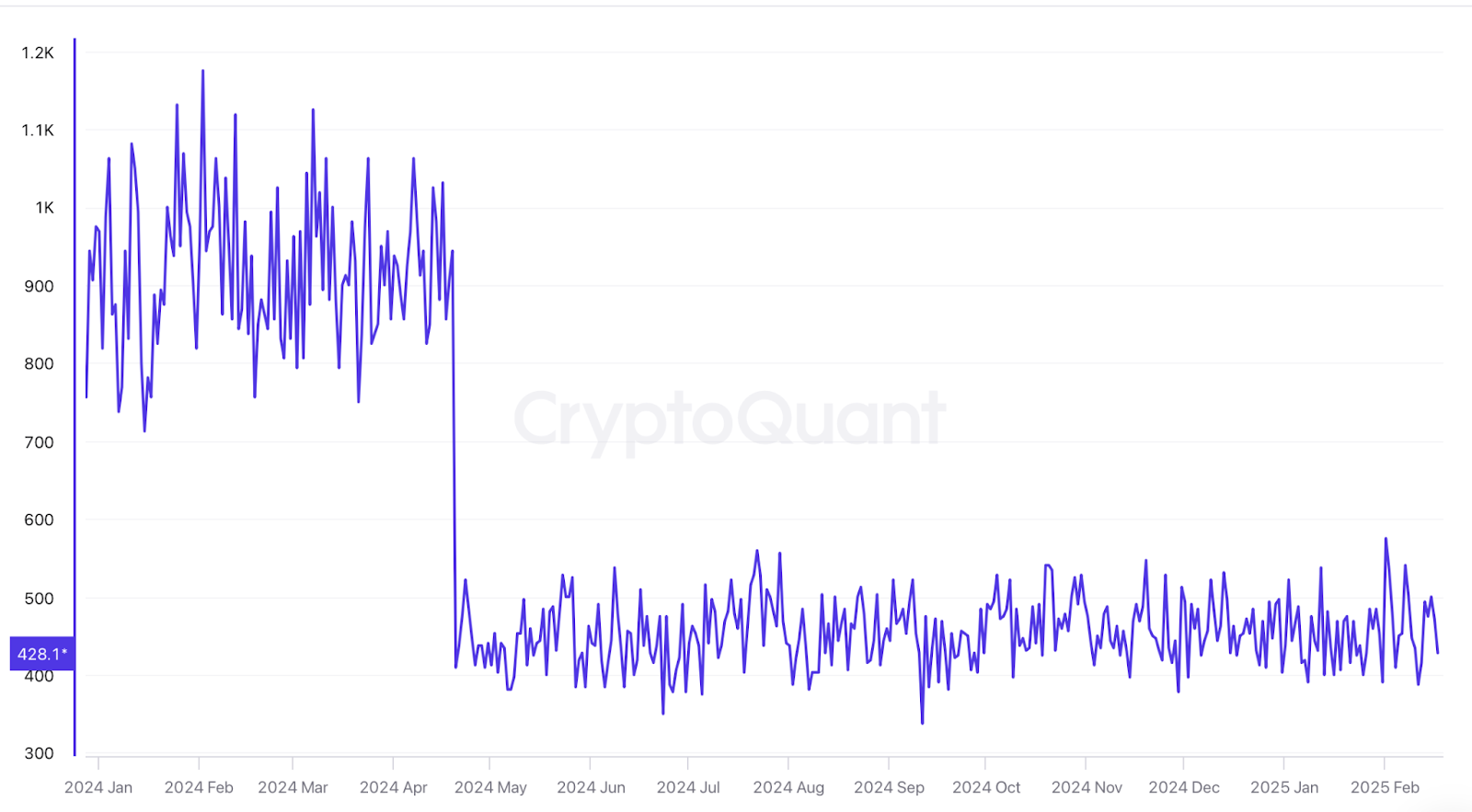

Since his launch, this is ETF Attractive With financial giants such as Blackrock, Grassscale and Fidelity, the net flow with financial giants exceeded $ 40 billion.

The increase in demand has absorbed bitcoins at an unprecedented rate, with daily ETF procurement ranges from 1,000 to 3,000 BTC – which exceeds about 500 new coins each day. This increasing supply deficit is making bitcoin rarely rare in the open market.

At the same time, the bitcoin exchange reserves have fallen to 2.5 million BTC, the lowest level in three years. More investors are withdrawing their holdings from exchanges, indicating a strong conviction in the long -term capacity of bitcoin, rather than considering it as a short -term trade.

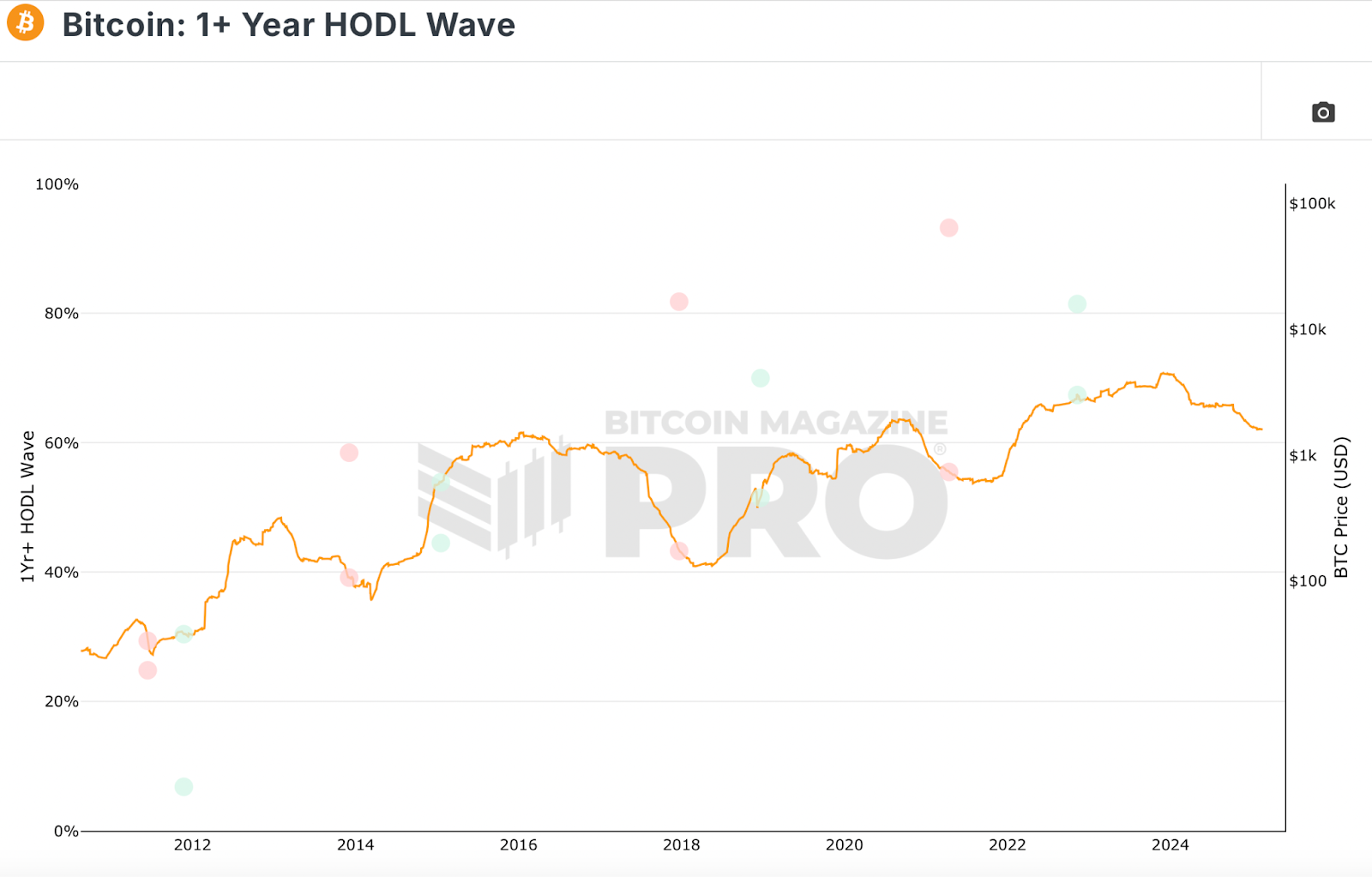

Taking forward this trend, long -term holders dominate the supply. As of December 2023, 71% of all bitcoins remained untouched for more than a year, highlighting deep investor commitment.

While this figure has decreased by 62% compared to February 18, the broader tendency points to bitcoin which has become a faster tightly held property over time.

Flipping is not coming – it’s here

By January 2025, middle American home-selling price Stand -up In $ 350,667, 7%is hovering with mortgage rates. This combination has pushed the monthly mortgage payment to record high, making home owners unattainable for young generations.

To keep it in perspective:

- 20% down payment at an average price house now exceeds $ 70,000-a figure that crosses the total domestic value of previous decades, in many cities.

- For the first time homebuits now represent only 24% of the total buyers, a historic Less Compared to a long-term average of 40%-50%.

- Total US domestic loan hostage has increased to $ 18.04 trillion Accounting For 70% of the total – to find out the growing financial burden of the homeowner.

Meanwhile, Bitcoin has improved real estate in the last decade, Proud A mixed annual growth rate of 102.36% since 2011 – Application for CAGR 5.5% of the housing in the same period.

But beyond the return, a deep generational change is coming out. Millennials and General Z, a digital-first-first in the world, see traditional financial systems as slow, rigid and old.

The idea of being owned by a decentralized, border property like bitcoin is much more attractive than being bound by 30 years of mortgage with unexpected property taxes, insurance costs and maintenance expenses.

Surveys suggest that young investors rapidly prioritize financial flexibility and dynamics on homeowners. Many people like to hire and prefer to keep their property liquid, instead of real estate illegality.

The resistance to the portability of bitcoin, round-the-clock trading, and sensorship is fully align with this mentality.

Does this mean that real estate is becoming obsolete? Not completely. It is a defense against inflation and a valuable property in high-deserves areas.

But the incapacity of the housing market – Combined with the increasing institutional acceptance of bitcoins – is re -shaping investment preferences. For the first time in history, a digital property is competing directly as a long -term store of value with physical real estate.

The question is no longer whether bitcoin is an alternative to real estate – how soon the investors will accommodate this new reality.